Prop Trading Strategies to Pass Evaluations and Scale Funded Accounts

On the other hand, a trader with a prop account must first perform successfully in the test or evaluation phase of prop trading firms and use the company’s capital that has been provided to them. In these types of accounts, profit is shared as a percentage between the trader and the prop firm, and the trader must use capital management rules and smaller leverage to protect the capital entrusted to them. For this reason, it is very important that, as a prop trader, you are aware of and proficient in the best prop trading strategies so that your chances of success in trading increase.

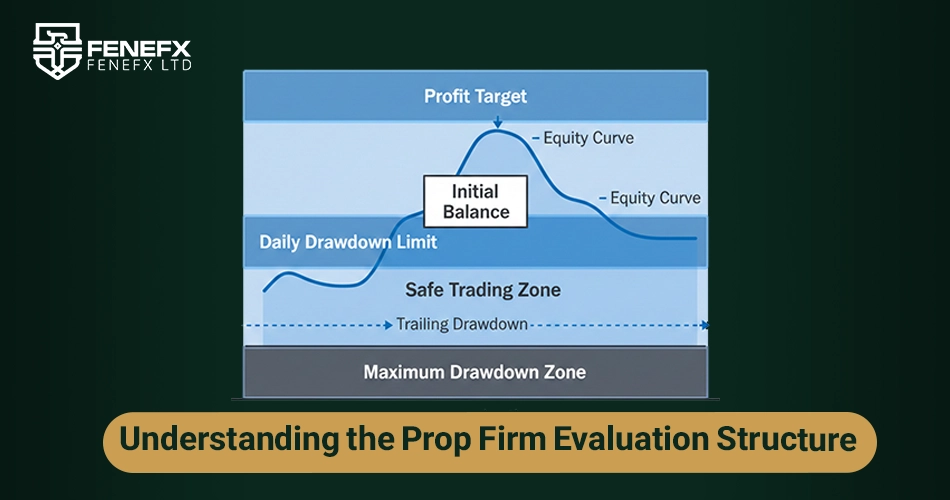

Understanding the Prop Firm Evaluation Structure

Before selecting any trading methodology, the structural mechanics of the evaluation phase must be fully understood.

Drawdown Limits and Capital Preservation Rules

Most proprietary firms impose strict daily and overall drawdown thresholds, predefined profit objectives, and leverage restrictions. These constraints are designed to test liquidity management and emotional control rather than speculative accuracy. Traders who breach drawdown parameters rarely do so because of poor market bias; more often, the failure stems from inadequate risk compression during volatility spikes.

Why Evaluation Is a Risk-Control Test, Not a Profit Contest

The evaluation stage functions as a behavioral audit. Firms assess whether a trader can maintain composure when price action accelerates, spreads widen, or market structure temporarily invalidates a setup. Those who treat the challenge as a race to the profit target frequently overexpose their capital and violate internal limits. Sustainable progression requires patience and structural alignment.

Breaking Down Prop Firm Rules and Structural Constraints

Understanding evaluation rules conceptually is insufficient. Traders must internalize the mechanical structure behind drawdown calculations and capital limits.

Daily vs Overall Drawdown Mechanics

Daily drawdown is typically calculated based on either balance or equity, depending on the firm’s model. A sudden volatility spike during a high-impact session can trigger equity-based breaches even if the trade eventually recovers.

Overall drawdown defines the maximum capital tolerance from the initial or peak balance. Once violated, the account is terminated regardless of long-term expectancy.

Professional traders operate with an internal buffer below firm thresholds. They rarely allow exposure to approach maximum limits.

Trailing Drawdown and Equity-Based Risk

Trailing drawdown models are particularly misunderstood. In many cases, the allowable loss level moves upward as equity increases. This creates a dynamic risk ceiling.

Aggressive early profit followed by a pullback can eliminate the account even if the trader remains net positive.

The strategic implication is clear: smooth equity progression is structurally safer than rapid expansion followed by volatility compression.

Position Limits and Scaling Policies

Some firms cap contract size or lot exposure relative to account growth. Scaling prematurely can distort risk metrics and increase slippage sensitivity.

A professional approach treats scaling as conditional, not automatic.

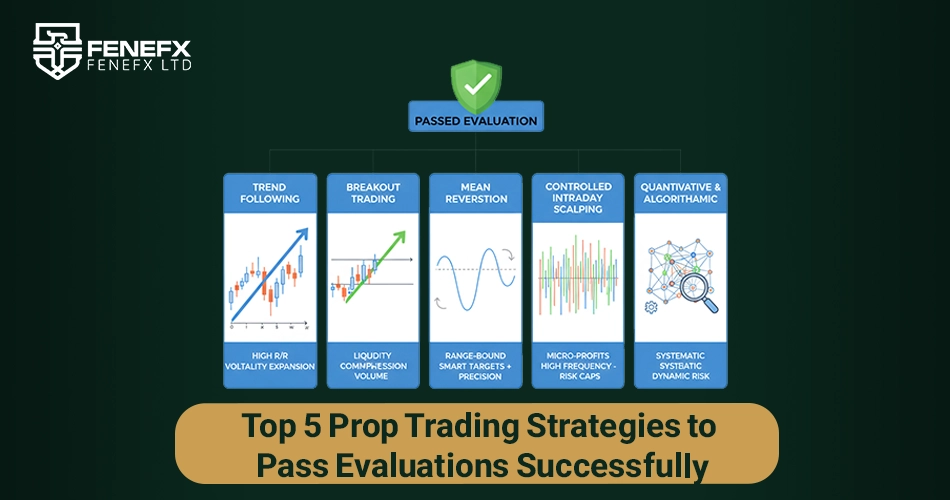

Top 5 Prop Trading Strategies to Pass Evaluations Successfully

Passing a prop firm evaluation requires selecting strategies that align with volatility regimes, liquidity conditions, and firm risk constraints. The following five approaches consistently appear across leading prop trading discussions and demonstrate structural compatibility with evaluation environments.

- Trend Following During Volatility Expansion

- Breakout Trading After Liquidity Compression

- Mean Reversion in Range-Bound Markets

- Controlled Intraday Scalping

- Quantitative and Algorithmic Execution Models

Trend Following During Volatility Expansion

Trend-following models demonstrate the highest structural efficiency during volatility expansion phases, when directional liquidity supports sustained price discovery. Rather than anticipating movement, professional execution focuses on confirmation of market structure shifts—typically a break of structure on higher timeframes followed by a retracement into support or resistance, supply-demand zones, or liquidity pools.

In evaluation accounts, this approach benefits from asymmetric risk-reward dynamics. When momentum aligns with higher-timeframe bias, trades can generate two to four times the initial risk, reducing the frequency required to meet profit objectives. This naturally limits exposure to daily drawdown thresholds. However, the strategy deteriorates rapidly during consolidation cycles. Overtrading in compressed ranges increases variance and compresses expectancy. Volatility-adjusted stop placement, calibrated to ATR or structural swing points, ensures that exposure remains proportionate to prevailing market conditions rather than emotional impulse.

Breakout Trading After Liquidity Compression

Breakout systems seek expansion following prolonged range contraction. Liquidity compression often manifests through narrowing ranges, declining ATR, and clustering around key resistance or support levels. When participation expands and order flow accelerates, price can transition rapidly into directional movement.

The challenge in prop evaluations lies in false breakouts. Thin liquidity conditions, session transitions, or pre-macro positioning frequently generate liquidity sweeps before true expansion unfolds. Confirmation through strong closes beyond structural levels and increasing volume participation improves reliability. Risk must be tightly controlled because repeated failed breakout attempts can quickly accumulate losses within strict daily limits. In accounts with trailing drawdown mechanics, early aggressive gains followed by failed breakout sequences can create structural vulnerability even while net equity remains positive.

Mean Reversion in Range-Bound Markets

When volatility contracts and directional conviction weakens, mean reversion becomes structurally viable. In low-volatility regimes, price tends to oscillate around equilibrium zones such as VWAP or value areas. Deviations beyond statistically stretched thresholds often revert as liquidity rebalances.

Within evaluation frameworks, mean reversion requires surgical precision. Profit targets are typically smaller, which increases sensitivity to transaction costs and slippage. Stop placement must be narrowly defined relative to range boundaries, and position sizing must remain conservative to avoid cumulative exposure. Emotional overreaction to temporary range breaks often destroys the statistical edge of this approach. Because trade frequency can increase in range environments, internal daily loss buffers below firm-imposed limits are essential to prevent incremental drawdown accumulation.

Controlled Intraday Scalping

Scalping strategies operate on micro-inefficiencies and short-duration price fluctuations. Their viability depends on liquidity depth, spread stability, and execution efficiency. Even marginal slippage can materially alter expectancy, particularly when risk-reward ratios are compressed.

In evaluation environments, this approach carries elevated structural risk. High trade frequency increases the probability of reaching daily drawdown caps, especially in accounts where equity is monitored intraday. Additionally, some firms restrict latency exploitation or excessive micro-duration trading. As a result, scalping must be tightly regulated, with predefined maximum trade counts, strict percentage-based risk allocation, and avoidance of high-impact news windows where spreads widen and liquidity temporarily evaporates.

Quantitative and Algorithmic Execution Models

Algorithmic and quantitative strategies introduce systematic discipline by removing discretionary bias. Models based on volatility clustering, statistical arbitrage, or macro-driven positioning can produce consistent execution if properly calibrated. Backtesting across multiple volatility regimes is essential to validate positive expectancy and to measure maximum drawdown distribution rather than focusing solely on net returns.

However, automation does not eliminate structural risk. Overfitting to historical data, failure to incorporate volatility regime shifts, or neglecting firm-specific exposure rules can rapidly invalidate otherwise profitable systems. Risk throttling mechanisms must dynamically reduce exposure during volatility spikes or liquidity fragmentation. Even in algorithmic environments, oversight remains necessary to ensure compliance with position limits and drawdown ceilings.

Strategy | Volatility Regime | Risk Profile | Suitable for Evaluation? | Main Risk |

| Trend Following | Expansion | Asymmetric RR | High | Overtrading in consolidation |

| Breakout | Post Compression | Momentum-based | Moderate | False breakouts |

| Mean Reversion | Low Volatility | Tight RR | Conditional | Range failure |

| Scalping | High Liquidity | Execution-sensitive | Limited | Slippage |

| Algorithmic | Variable | Model-dependent | Advanced | Over-automation |

Psychological Capital in Prop Evaluations

Capital is not only financial. It is psychological.

Managing Performance Anxiety Under Drawdown

Evaluation pressure intensifies when approaching drawdown limits. Traders often tighten stops excessively or widen them impulsively. Both reactions distort system expectancy.

Structured breathing space after losses preserves decision clarity. Reduced exposure during emotional volatility is not weakness; it is risk calibration.

Avoiding Strategy Switching After Variance

Short-term variance is statistically inevitable. Strategy abandonment after two or three consecutive losses indicates structural fragility.

Edge validation requires patience across sample size. A disciplined trader evaluates performance through distribution, not emotion.

Risk Management as the Structural Core

All reviewed sources converge on one fundamental truth: risk control determines survival. Without structural risk discipline, even statistically sound systems collapse under volatility pressure.

Position Sizing Framework

Professional capital management involves consistent percentage-based risk allocation per trade, predefined daily exposure caps below firm-imposed thresholds, and careful avoidance of correlated positions that amplify aggregate drawdown.

Managing Drawdown Under Volatility Expansion

During volatility spikes, exposure must be reduced rather than increased. Emotional escalation following losses often leads to compounding errors. Temporarily stepping aside after structural drawdowns preserves both capital and psychological clarity.

Example Risk Model for a $100,000 Prop Account

Before applying any strategy, traders must define a structured risk framework. Below is a conservative capital allocation model aligned with common prop firm drawdown constraints

| .Parameter | Conservative Model |

| Risk per Trade | 0.5% ($500) |

| Daily Max Risk | 2% ($2,000) |

| Max Simultaneous Trades | 2 |

| Weekly Loss Cap | 4% |

| Target RR | Minimum 1:2 |

Adapting Strategies to Prop Firm Constraints

Propiy’s emphasis on contextual awareness highlights the necessity of aligning strategy mechanics with rule frameworks.

Modifying Strategy for Rule Compliance

Holding periods may require adjustment if overnight exposure is restricted. Risk-reward parameters may need recalibration to align with daily loss limits. News exposure policies may necessitate reduced activity during high-impact events.

Aligning Risk-Reward With Drawdown Limits

Smooth equity progression is more valuable than rapid capital acceleration. Evaluation systems reward stability and risk compression more than episodic profitability.

Building a Structured Evaluation Game Plan

Passing an evaluation requires phased execution rather than random trade accumulation.

Phase 1: Capital Preservation

The first objective is stability. Exposure remains conservative until a structural profit cushion forms. Avoiding drawdown breaches takes priority over rapid growth.

Phase 2: Controlled Expansion

Once a buffer exists, risk can increase moderately within firm limits. Trade selection becomes more selective, focusing on high-conviction setups.

Phase 3: Scaling After Cushion

Scaling should only occur when equity expansion demonstrates statistical stability. Premature scaling increases structural risk and emotional exposure.

Advanced and Quantitative Approaches

Goat Funded Trader discusses algorithmic and quantitative strategies that extend beyond discretionary execution.

Algorithmic Execution Models

Quantitative systems analyze volatility clustering, liquidity dislocations, and statistical arbitrage opportunities. When properly structured, algorithmic models can enhance consistency.

Risks of Over-Automation

Automation without risk throttling can magnify slippage and violate internal firm constraints. Even algorithmic systems require human oversight to adapt to structural market shifts.

News Awareness and Volatility Management

Blackwell Global emphasizes the importance of macroeconomic awareness in prop trading environments.

Trading Around Economic Releases

High-impact economic data releases generate temporary liquidity vacuums and spread expansion. Exposure during these moments must be calibrated carefully to avoid premature stop-outs.

Volatility as Opportunity and Threat

Volatility expansion offers directional opportunity, yet unmanaged exposure during unstable conditions accelerates drawdown breaches. Professional traders recognize when participation probability declines.

Common Structural Mistakes in Prop Evaluations

Across the referenced platforms, several recurring behavioral errors appear. Traders frequently increase leverage to accelerate target attainment, abandon tested systems after short-term variance, or engage in emotional retaliation trading following losses. These behaviors undermine structural stability.

Consistency, not intensity, defines sustainable evaluation success.

Maintaining Edge Across Market Cycles

Markets transition between volatility expansion and compression. Liquidity rotates between sessions and asset classes.

Volatility Regime Shifts

A strategy optimized for high momentum conditions may underperform during consolidation cycles. Professional traders reduce exposure or switch structural bias when volatility contracts.

Liquidity Rotation Between Sessions

Session overlaps generate deeper liquidity and tighter spreads. Off-session environments increase slippage risk and false break probability.

Edge sustainability depends on adaptability, not rigidity.

Final : Strategy Is a Dynamic Process

A failed evaluation does not indicate incapability. More often, the strategy was misaligned with structural constraints or improperly calibrated for prevailing volatility conditions.

If a method repeatedly collapses under drawdown pressure, the framework must evolve. Markets transition through liquidity cycles and volatility phases. Adaptation is not optional; it is a prerequisite for long term survival in proprietary trading environments.

.Frequently Asked Questions

1.What is the safest strategy to pass a prop firm challenge?

A low risk trend following or structured breakout model with strict drawdown control is statistically safer than aggressive scalping.

2.How much should I risk per trade in a prop firm?

Most professional traders risk between 0.5% and 1% per trade to avoid breaching daily drawdown limits.

3.What happens if I hit the daily drawdown limit?

The account is typically terminated immediately, regardless of unrealized recovery potential.

4.Is scalping allowed in prop firms?

It depends on the firm. Some restrict latency-based or high-frequency execution models

5.How long does it take to pass a prop evaluation?

Most traders pass within 10–30 trading days if they maintain structured risk discipline.

Comments

Any advice on adjusting risk in phase 2 when the profit target drops? Would love a follow-up on funded-account scaling plans too.

Solid, realistic advice — rare for this topic.

The section on treating the eval like a marathon instead of a sprint hit home. I've been rushing to hit targets in week one every single time. Thanks for this.

Failed two challenges overtrading NY session scalps. Switched to two swing setups a week and passed on the third attempt with days to spare. Slowing down was the whole trick for me.

After passing a few evals, my honest take: the strategy matters less than people think. Consistent risk per trade and knowing when NOT to trade is what actually gets you through. Boring wins.